Up-to 4% leakage due to commissions, costs and other inefficiencies

Most people have a retirement account and a 401K account through which they are funding their retirement. The expectation is that it is managed by professionals and hence is doing well relative to the markets.

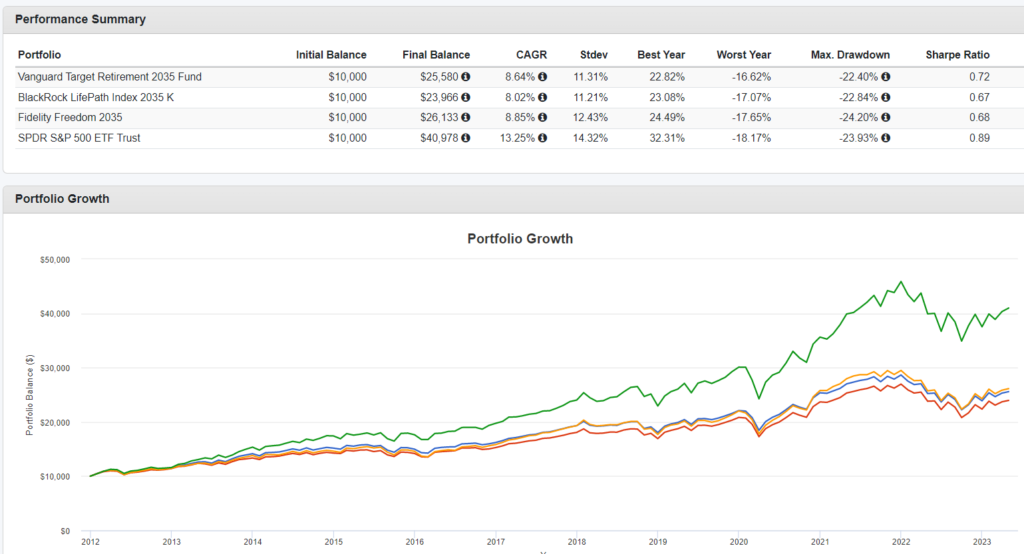

Here is data that proves otherwise. We took data from three popular providers and compared that to the S&P 500 over time.

As you can see from the graph and the table, most target retirement accounts have a similar risk to the S&P 500 and a 4% annual drop in performance compared to the index. Cumulated over time, that adds up to quite a dollar amount over time.

Where is this money going?

The leakage is primarily due to inefficiencies built in the system. When you invest in a 401K account, you are paying a manager of the target retirement fund, who in turn is using other mutual funds from his organization; with each mutual fund paying its managers. The distance between a target retirement fund and the final stock it is investing in involves a number of investment managers who are charging expenses. The data seems to show that this leakage adds up quite significantly.

What can you do about it?

The easiest thing to do is to take control and instead of depending on a target retirement fund, use ETF’s or index funds to allocate your money. You cannot do worse than the target retirement funds; as long as you are investing in index funds.

If you have the bandwidth and the ability to be more active, use one of the strategies that we had highlighted earlier here to do better than the index. There are other strategies as well which require less than an hour every year to do some analysis and rebalance your portfolio. Contact us to learn more.

What if you do not have the bandwidth? Or do not trust your emotions?

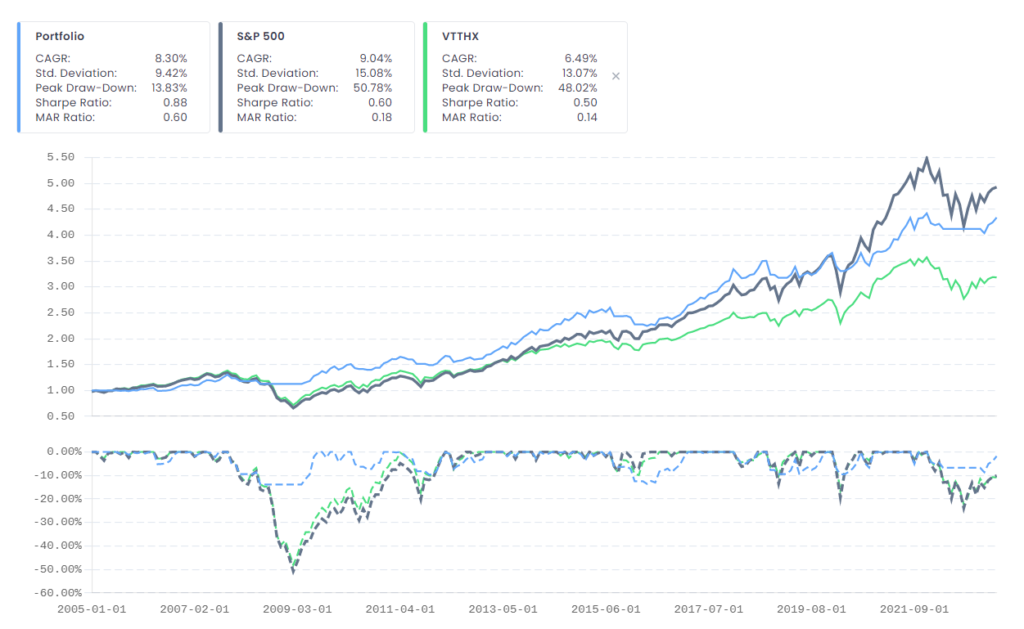

Another option would be to let us manage your company 401K account. Thanks to a partnership we just signed, we now have the ability to actively manage 401K retirement accounts that are company provided on an active basis using our AI tool Darwin. The performance would depend on the options available in your company 401K; but assuming the basic minimum of index mutual funds or ETF’s; here is how Darwin would have beaten the performance of a Vanguard target retirement fund (VTTHX is Vanguard’s 2035 retirement fund)

The first chart above is how a dollar invested would have grown in the three options. Black representing the S&P 500. Blue representing Darwin assisted investing and the green line representing the Vanguard target retirement fund. Also note that in 2008-2009; both the S&P 500 and the Vanguard models dropped by 50%; whereas the Darwin assisted models dropped only by around 15%

Keep in mind though that if your company 401K provider has other risk-off options like bonds, gold, commodities etc., the performance is even better.

What or Who is Darwin?

All Stocks will go bankrupt, and all stock picking strategies will fail…

That is the going in assumption behind Darwin, our AI model for portfolio management. Darwin is from mystockdna, our affiliate firm; a collaboration between academics, technology and finance professionals.

As a by-product of managing risk, can you achieve higher returns than the S&P 500?

Darwin strives to do this via an “evolutionary” approach where assets compete for allocation in a portfolio, akin to players vying for selection in a sports team. However, once assets are included in the portfolio, they work together to achieve the goal of winning. By increasing allocation to better performing players and reducing allocation to weaker players, Darwin is designed to reward consistency and prioritize lower risk-taking in pursuit of returns.