Understanding Returns and Risk

Imagine a highway consisting of three lanes – the slow lane, middle lane and the fast lane.

Which lane would you take to get to your destination?

All lanes will have the potential to get you to your destination, but each lane has a different speed and the associated risk of “accidents”

Consider those three lanes to be stocks, bonds and gold.

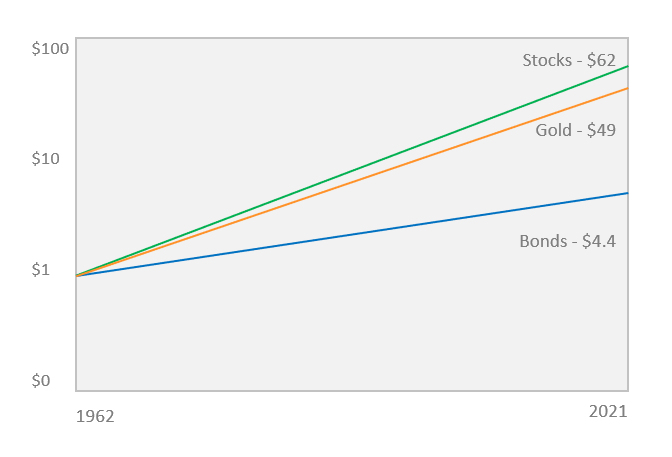

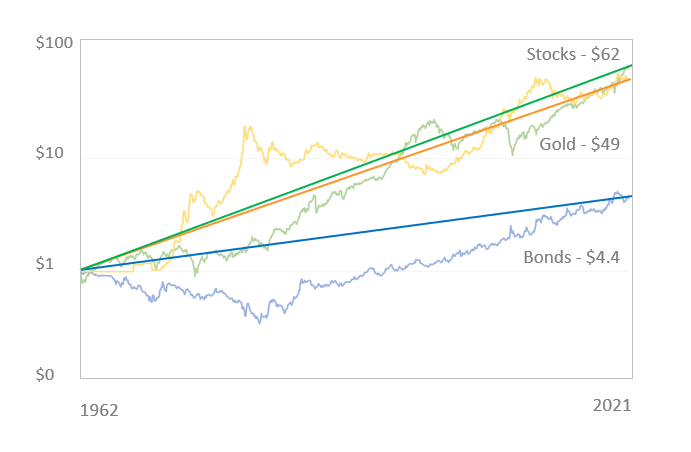

A dollar invested in 1962 would have turned into $62 by 2021 if it was invested in stocks (S&P 500)

A dollar invested in bonds (20+ year treasury bonds) would have turned into $4.4

A dollar invested in gold would have turned into $49

Unlike interest on fixed deposits, the returns on each asset would not be a straight line and involve a lot of turbulence.

All assets would have the potential to make you money just like all lanes will eventually get you to your destination, but each lane has a different speed and “risk” of turbulence.

Bonds for example had the least turbulence, followed by stocks and then gold

Between 1962 to 2021, for stocks, the maximum turbulence quantified as risk would have been the 50% drop in the 2008-2009 time-frame. This risk measure is called the peak drawdown.

The average annual return for the stock market being ~9%, that would give us a return to risk ratio of ~0.15-0.20

The goal of any good portfolio should be to maximize the return and minimize the turbulence it takes to get that return.

In other words, the goal is to maximize the return to risk ratio.

Asset Diversification

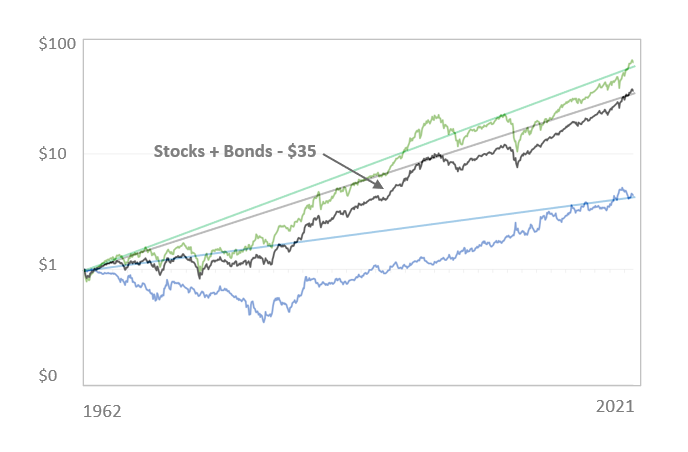

One way of reducing turbulence (risk) is by switching lanes (diversifying across assets).

Combining stocks and bonds for example would have reduced the returns slightly but would significantly reduce the turbulence (risk) to a drawdown of 20-25% in the 2008-2009 time-frame.

A return to risk ratio of ~0.30-0.40

Time Diversification

We use the term Time Diversification to describe our unique approach where we also diversify between different strategies including long term, swing trading and day trading models.

This helps us seek to avoid large drops in the market and potentially even make higher returns when the market drops

Asset Diversification + Time Diversification

Imagine being stuck in slow traffic and envying that bike rider weave through traffic

What if you could not just switch lanes (diversify between assets), but also switch vehicles (diversify between various strategies)?

Our models target a higher return per unit risk taken because of this unique diversification approach